Add to favorites

What is the tourist tax?

The tourist tax helps finance expenses intended to promote the territory and therefore encourage visits to the Pays d'Angoulême.

The greater the tourist tax revenue, the greater the possibilities for action and the more ambitious the activities of the tourist office will be. Advertising, promotional actions, the quality of the welcome in the broad sense, attract tourists.

It is therefore a WIN/WIN operation with tourism providers to maintain the virtuous circle of sustainable tourism development.

Who decides on the tourist tax?

As a reminder, the tourist tax was standardized at the same amounts in all the municipalities of GrandAngoulême then following deliberations of the Community Council.

It concerns all the municipalities of the intercommunality whose tourism competence has been transferred under the NOTRE Law.

Who pays it?

People who are not residents of the territory and accommodated for a fee.

Therefore, it is up to the customer to pay extra and not up to the service provider to include the tourist tax in their sales price.

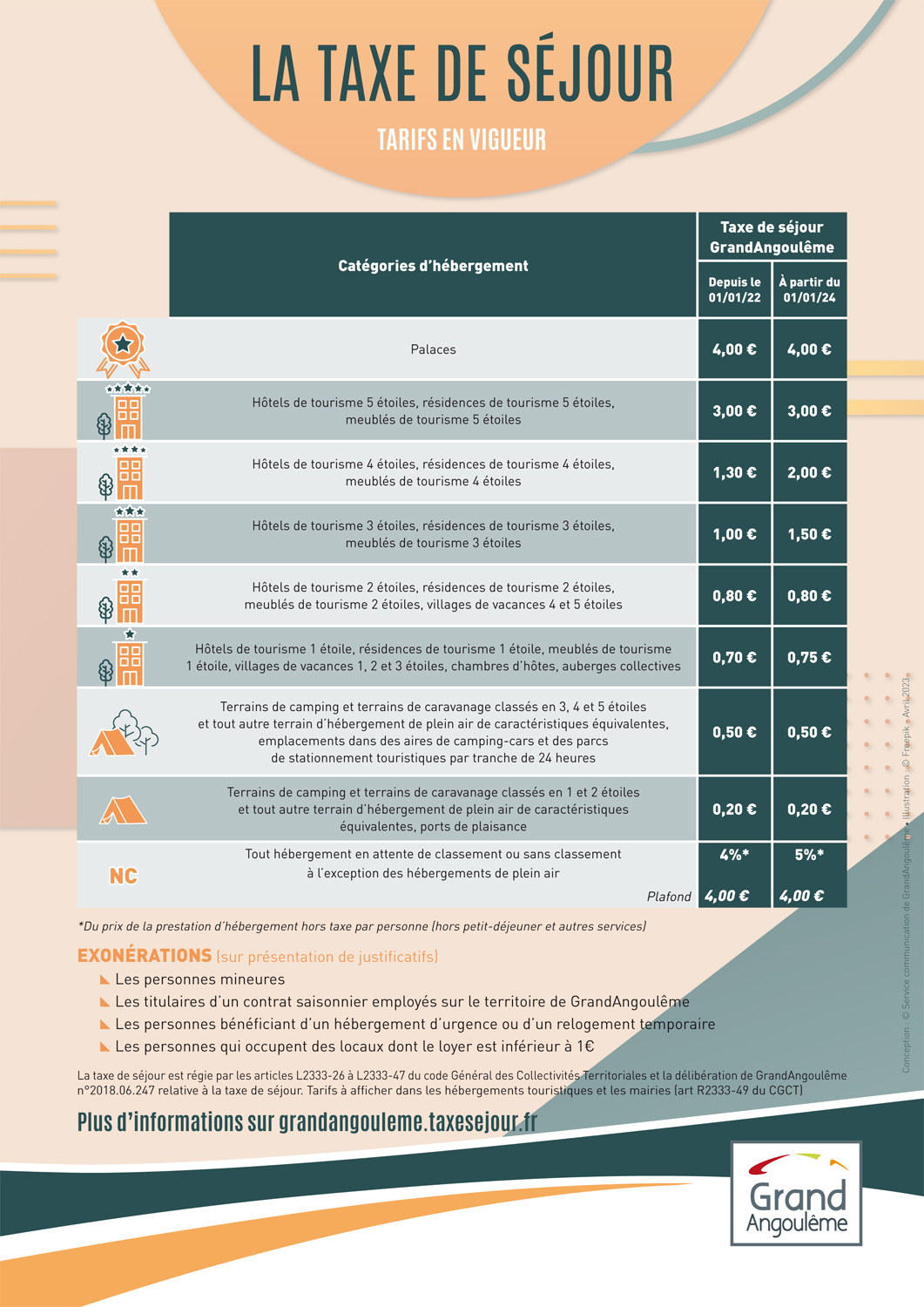

Exemption cases:

– Minors (under 18 years old)

– Holders of a seasonal employment contract employed in the territory of the GrandAngoulême agglomeration community

– People who occupy premises whose weekly rent is less than an amount that the community council has determined

– People benefiting from emergency accommodation or temporary rehousing. Therefore, salespeople, festival-goers, interns or employees on mission are subject to it.

The obligations of the host

Accommodators have an intermediary role in the recovery of the tourist tax and are subject to a certain number of commitments:

– Report to the town hall as a paid host online or with CERFA depending on the activity declared: rental: No. 1400404, guest room: No. 1356603

– Display the tourist tax rates in the reception area, visible to the customer (see document to download)

– Include the tourist tax on the reservation contract then on the invoice given to the customer. Thanks to this principle, tourists can easily identify its impact on the price of their stay. The tourist tax is not subject to VAT.

– Declare the amounts collected on the dedicated platform per accommodation and per period

Who collects it?

The host collects the tourist tax: it is he who collects the amount from the customer except in exceptional cases of online agencies (OTA): Booking, Airbnb, Leboncoin, Gîtes de France, etc.

He must pay the entire tourist tax back to his community. It is collected throughout the calendar year (from January 1 to December 31).

What are the amounts?

The amount of the tourist tax depends on the category and classification of the accommodation. They are voted on by communities based on the floors and ceilings communicated each year by the state.

Should we cash customer checks?

The accommodation providers collect the tourist tax then remit it to the community by bank card, transfer or direct debit via https://grandangouleme.taxesejour.fr/ or by check sent by post with a declaration statement

Declaration

Ideally, the amounts collected each month should be reported on the platform without forgetting the exemptions: OTA (booking, Airbnb, Gîtes de France), children, etc.

How often should payments be made?

The deadlines are defined by the deliberations of the communities which introduced the tourist tax.

What payment methods?

It is advisable to remit the tourist tax by credit card or bank transfer on the dedicated platform.

What is the sanction in the event of non-payment?

In the event of absence of declaration, incorrect declaration or late payment of the tourist tax collected, the executive of the community sends the owner a formal notice by registered letter with request for acknowledgment of receipt.

In the absence of regularization within the period of thirty days following notification of this formal notice, a reasoned tax notice is sent to the defaulting declarant.

In the event of failure to repay, a fine of €750 to €2500 may be added to the financial penalty of 0.20% of the amount due per month of delay.

Example of calculation for unclassified

Price per night excluding tax x 5% (rate to apply) / Number of nights * Number of persons subject to tax

The classification of accommodation

It may be wise to classify rental accommodation to avoid complicated calculations for the customer and the service provider!

Especially since the ranking allows the host to benefit from several advantages:

– It is a guarantee of quality

– It allows you to benefit from an additional tax reduction

– It allows you to accept holiday vouchers

– It allows optimized display on the websites of tourist offices and Charentes Tourisme.